Monday is all about academic (and practitioner) literature at Abnormal Returns. You can check out last week’s links including a look at the value (or not) of the Sharpe Ratio.

Anomalies

- How investors affect the returns to the low vol anomaly. (blog.alphaarchitect.com)

- Is there an exploitable earnings announcement anomaly? (blog.alphaarchitect.com)

- Some smart beta factor timing makes sense in the framework of diversification. (researchaffiliates.com)

Research

- Asset allocation trumps stock selection. (gestaltu.com)

- Month-end-effects and the performance of tactical strategies. (allocatesmartly.com)

- Are asset class correlations rising due to the popularity of ETPs? (capitalspectator.com)

- How to use buyback signals. (investingresearch.net)

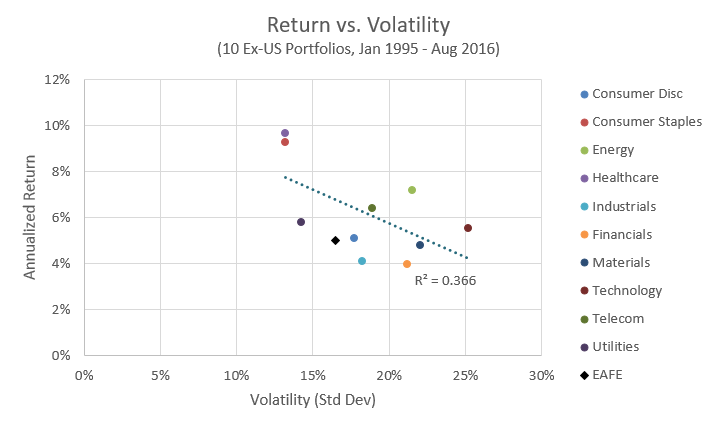

- A review of recent research on volatility. (capitalspectator.com)

- Institutional traders do seem to have some trading skill. (papers.ssrn.com)

- Why do new mutual funds succeed? (morningstar.com)

- Making the case for P2P loans as an asset class. (etf.com)

- Options pricing methodologies from the 19th century. (quantpedia.com)

- How CEO personality affects firm policies. (papers.ssrn.com)