Tuesdays are all about academic (and practitioner) literature at Abnormal Returns. You can check out last week’s links including a look at papers presented at the Fall Q-Group conference.

Quote of the Day

"In the school of hard knocks, experience helps us be grounded in reality. Perhaps this is what you should be asking for from an experienced manager, a measure of reality that they may not always be successful, drawdowns will happen, and their estimates of what they will be able to achieve are close to what can be produced. Reality and learning leads to less overconfidence and perhaps better long-term returns."

(Mark Rzepcynski)

Research links

- Momentum investing is not growth investing. (charlessizemore.com)

- Great minds disagree on the source of the value premium. (blog.alphaarchitect.com)

- The role leverage plays in the low vol anomaly. (quantpedia.com)

- A deep dive into the theoretical and practical implications of the equity risk premium. (nbim.no)

- Do Morningstar star ratings predict future performance? No so much. (beta.morningstar.com)

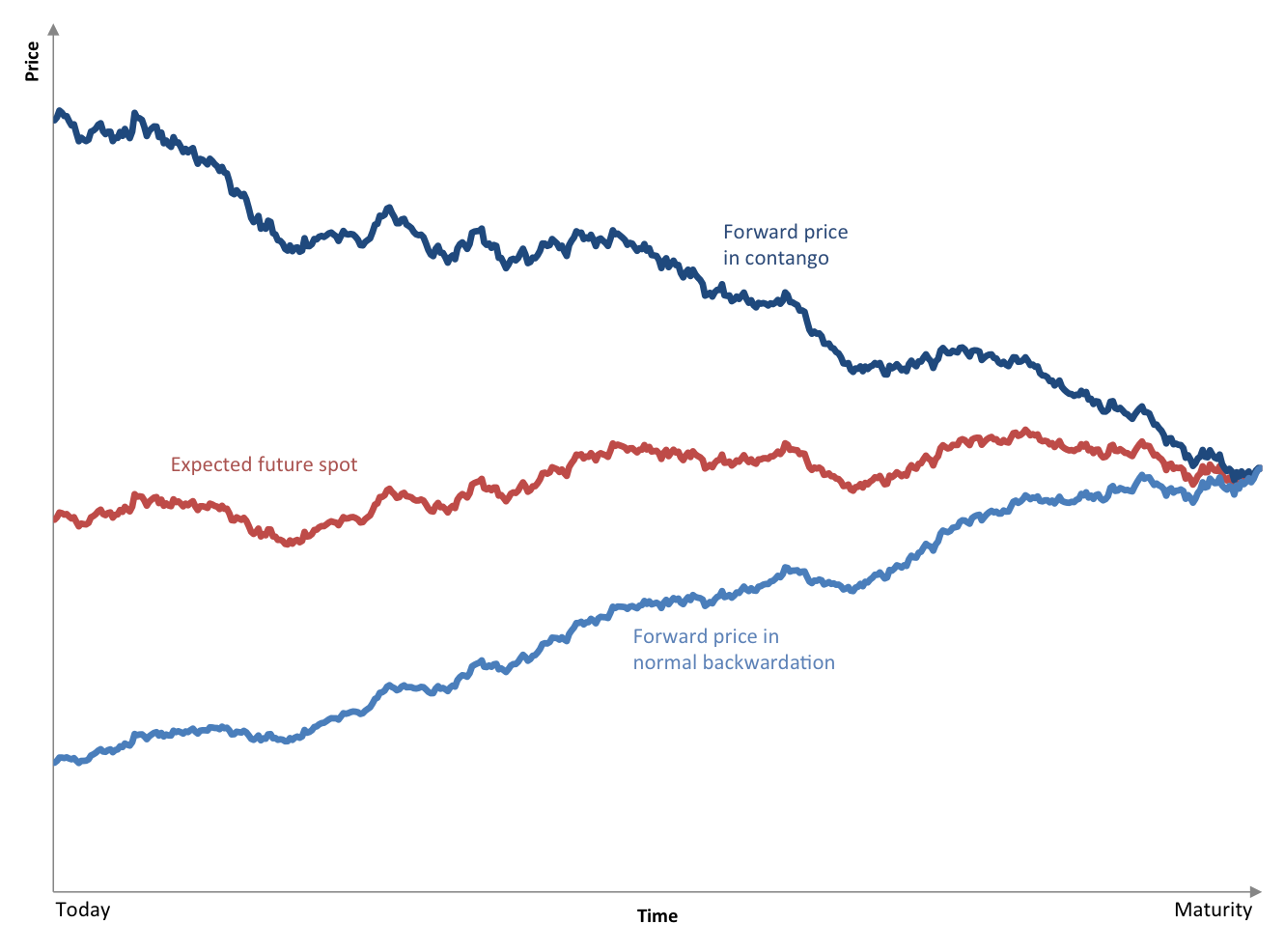

- Another look at the case for commodities as a strategic asset class. (papers.ssrn.com)

- How index funds lose during index changes. (papers.ssrn.com)

- A Q&A with Larry Swedroe co-author of "Your Complete Guide To Factor Investing." (etf.com)

- CEO incentive plans don't change as much over their tenure as you would think. (papers.ssrn.com)

- Women have not made gains in the fund management industry. (corporate1.morningstar.com)

- A stylized history of quantitative finance from Emanuel Derman. (ritholtz.com)