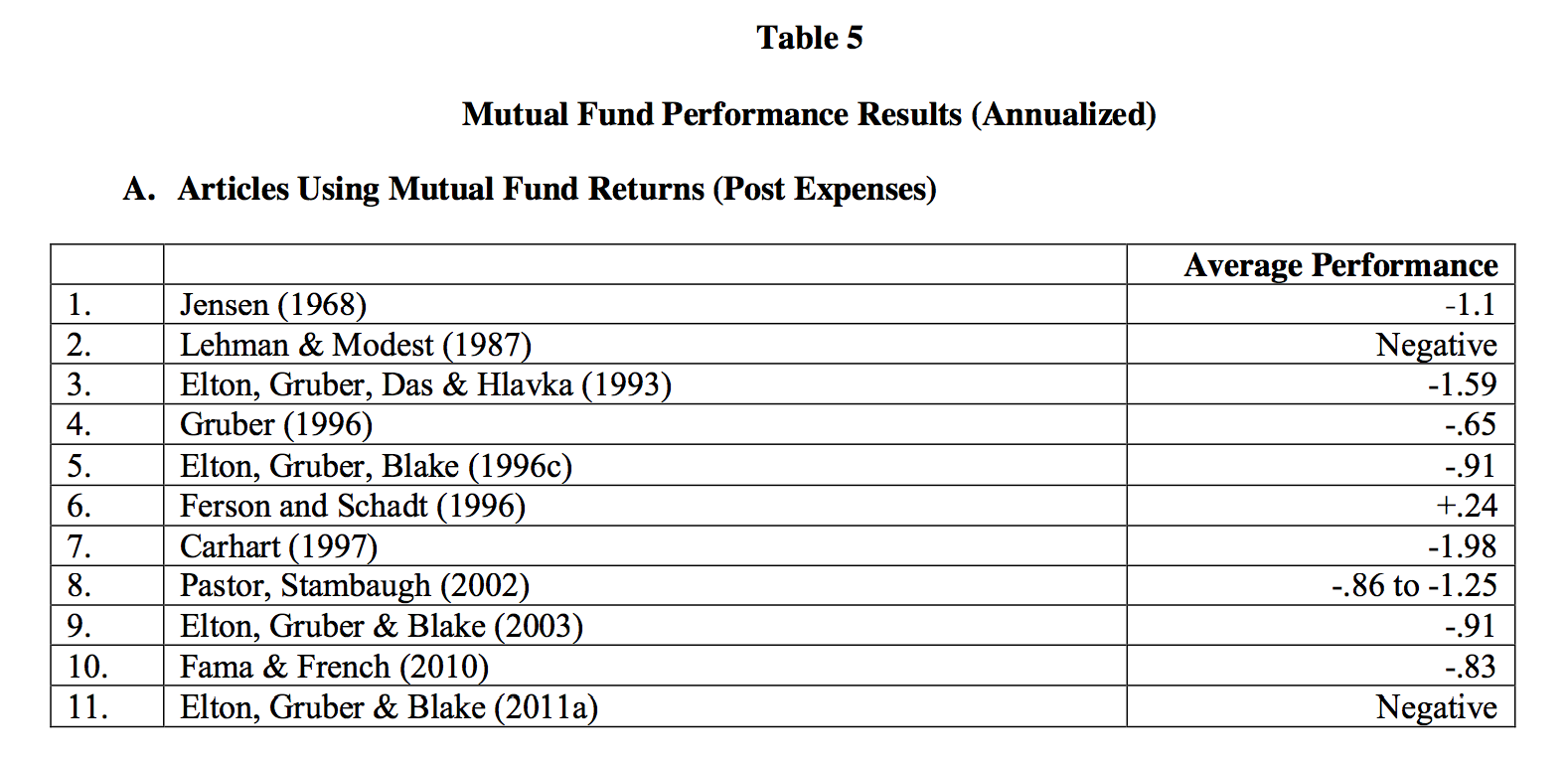

Now that the individual investor seems to be once again interested in equities the idea of picking actively managed mutual funds will once again become a media theme. This despite the fact that nearly every study of mutual fund performance has shown that on average actively managed mutual funds after expenses underperform their respective benchmarks.

Source: Elton and Gruber, “Mutual Funds” at SSRN for more data.

The interest in actively managed funds will inevitably increase. The financial media will help feed this desire to “beat the market.” This is due in part because investors seem to really only care about up-market outpeformance. A recent study shows that mutual funds that outperform in bull markets pull in more funds than those that outperform during down markets. In short, investors want to try and juice their returns in bull markets.

Given that is the case is there any guidance we can provide investors seeking out actively managed funds? Luckily a handful of articles discuss the very topic.

Barry Ritholtz at the Big Picture wisely notes that most investors would do best in index funds, but highlights a couple of things to keep in mind when selecting actively managed funds:

If you want to at last have a fighting chance to pick a fund that actually has a shot to beat its benchmark, these 2 steps are a start:

1. Low Fees — look for funds with an expense ratio of 0.86% or below.

2. Avoid Closet Indexers — find funds with a low R-squared ratio.

Low fees are the one variable that has consistently been shown to discriminate among fund performance. The math is pretty simple high fees monotonically reduce returns. The only thing worse than paying highs is paying highs for index-like performance. Michael Mauboussin writing at Marketwatch notes that a fund manager’s “active share” tells you a lot about how they manage their fund. He writes:

1. Look for funds with high ‘active share’

In order to generate returns higher than an index, a fund has to be different than the index. “Active share” is the percentage of the fund that differs from the benchmark index. Active share is 0% if the fund perfectly mirrors the index and 100% if it is totally dissimilar.

Think of active share as a proxy for stock picking. An active share of 60% or less is considered to be closet indexing and an active share of 90% or more indicates a manager who is truly picking stocks. Active share is highly persistent, which means it indicates skill.

Mauboussin also mentions low fees and correctly notes that focusing on a manager’s process is just as important as their actual returns. This is due in part to the fact that the fund returns we see are some mix of luck and skill that we really can’t decode in real-time. As per The Economist:

The difficulties facing investors when selecting individual mutual-fund managers are well known. Past returns may be a result of luck, not skill, and a smart manager may be hired away by a rival firm. But perhaps past data can still be of some use for asset-allocation purposes, if only as a contrarian indicator?

They find that in the short-run fund momentum tends to continue, however in the long-run mean reversion kicks in and those funds that performed worse tend to rebound. In that light active fund selection becomes an ongoing effort that requires investors to monitor performance and try to decode the offsetting effects of momentum and mean reversion. That is no small task. That is maybe why we continue to see a persistent gap between fund performance and actual investor performance, hence the “behavior gap.”

Picking actively managed funds requires investors to make a great deal more decisions than they would if they simply stuck to index funds. The media is going to start pumping up the volume on actively managed funds. Investors will feel left out if they didn’t own that one fund that blasted the market. However it is up to the investor to keep the many challenges involved in mind as they go about their investing lives.

Items mentioned:

Lipper Fund Flows: Equity Mutual Fund Flows Hit Levels Unseen in Nearly 12 Years. (AlphaNow)

Elton and Gruber, “Mutual Funds.” ( SSRN)

Gottesman, Morey and Rosenberg, “Outperformance, Underperformance and Mutual Fund Flows in up and down Markets.” (SSRN)

Finding Mutual Fund Managers Who Beat the Market. (Big Picture)

5 ways to be the best investor you can be. (Marketwatch)

The best, the worst and the ugly. (Economist)

Mind the gap: Why investors lag funds. (Morningstar)

Berkowitz seeking patient capital, sours on mutual funds. (Bloomberg)