A recent paper by Cam Harvey and his co-authors on the statistical validity of many so-called finance anomalies has attracted a great deal of attention in quantitative finance crowd. It seemed worthwhile to discuss the implications of the paper with one of our favorite quants, Wes Gray of Alpha Architect and manager of the ValueShares US Quantitative Value ETF ($QVAL) and the ValueShares International Quantitative Value ETF ($IVAL). Our questions appear in bold and Wes’ answers follow. Stay tuned for part two of our Q&A tomorrow.

————–

AR: I now do a linkfest each week focused on academic, or academic-inspired, research. You guys at Alpha Architect cover this area as well. Do you think the pace of academic research on investment strategies, anomalies, etc. is accelerating, stagnant or somewhere in between?

WG: You can only write about value investing and momentum investing so many times over before the academic journal editors finally say, “enough.” At this stage, I think most “anomaly papers”–save some one-off exceptions–have been published. But that said, there is no shortage of smart academics in search of new ideas in finance. As you well know, the pressure to publish is intense at top-tier research universities and the acceptance rates on top journals are getting below 5 percent. Not too long ago, the hit rate was around 10 percent. I think this decrease in acceptance rate reflects 2 trends: stronger competition and fewer novel ideas.

Stronger competition is typically a good thing–what gets published is typically higher quality. However, I think we’re seeing fewer novel ideas, which is a bad thing. Having followed academic finance research for over 15 years now, I’ve seen it evolve from novel ideas applied to novel datasets, to esoteric ideas applied to esoteric datasets. Computing power has opened the field and all the lowest hanging fruit associated with new datasets has been eaten. So while the pace of research has been strong over the past 20 years, it’s becoming more difficult to “move the needle” within the academic and research community.

Speaking to “anomaly research” in particular, academics have thoroughly investigated most of these anomalies. Also, from a cultural standpoint, it is somewhat taboo to write about market inefficiencies and conduct “anomaly chasing.” The recent Cam Harvey, Yan Liu, and Heqing Zhu paper actually mocks the practice of anomaly chasing with their appropriately titled paper, “…And the Cross-Section of Stock Returns.” It’s safe to say that making an academic career out of publishing papers based on so-called profitable trading strategies are numbered.

AR: As you mentioned, Cam Harvey and his co-authors recently published a paper essentially saying that most academic research is tainted by the issue of data mining. That is researchers are all rooting around in the same pool of now, well-examined data. How do you read this paper?

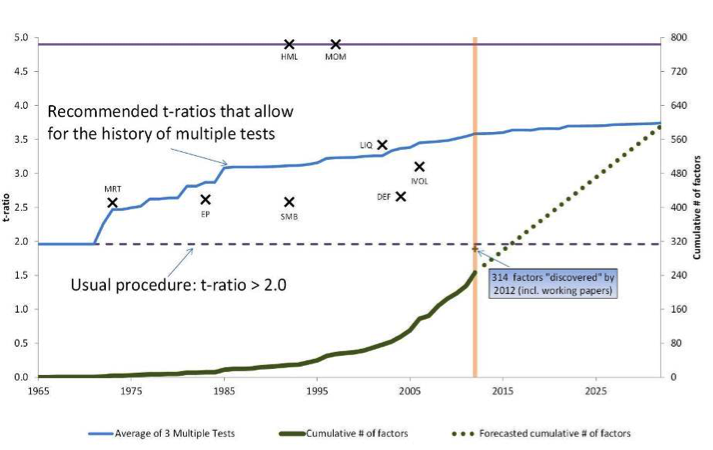

WG: It’s funny you mention that paper, since one of my partners–David Foulke–just bought me a t-shirt with the summary graphic from that paper printed across the front. The image is presented below.

Source: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2249314

The authors map out the “adjusted T-Stat” over time and show how various anomalies stack up. You’ll notice that value and momentum are well above “random chance” findings.

I’ve got a war-chest of geeky t-shirts, but I wear that shirt proudly around the office more often than not. I really love that paper. The one thing the paper highlights is how the statistical bar to be crowned an “anomaly” has been raised, because we need to consider the fact that academic researchers have been rooting around in the data for a long time.

AR: It is interesting that two of the three strategies to still remain robust after taking into account data mining issues are value and momentum. In Chapter 2 of my 2012 book, Abnormal Returns: Winning Strategies from the Frontlines of the Investment Blogosphere, I wrote about both of these so-called anomalies calling them enduring in part because they were both “psychologically difficult to follow.” I recommended investors combine the two approaches even though they appealed to two very different types of investors. Does this make sense?

WG: Agree 100% and I think you call it correctly in your book. A lot of folks think that I have a strong preference for value investing because I wrote Quantitative Value. And don’t get me wrong, I LOVE value-investing, but it is important to point out that I also wrote the foreword for Gary Antonacci’s book, Dual Momentum Investing, and I’ve done a lot of research on momentum stock selection strategies. So I’m clearly a fan of momentum-investing as well. To put it bluntly, I’m a fan of anything that has a good chance of compounding at high risk-adjusted rates (high benefit), but requires an investor to have a 5+ year horizon to be successful (dramatically limits competition).

The evidence is pretty clear that combining value and momentum is a good idea. Value and momentum are not perfectly correlated, giving investors diversification benefits, and thus a smoother overall return path, which tends to reduce volatility and psychological pain. One of my partners, and fellow PhD finance geek, Jack Vogel, has been burning a ton of midnight oil creating solutions in the momentum investing space. He recently wrote up a nice post a few months ago highlighting the clear benefits of combining active exposures to both value AND momentum.

————–

Be sure to check in with us tomorrow for the second part of our Q&A with Wesley Gray of Alpha Architect.