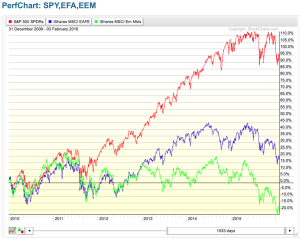

We have long been advocates of globally diversified, low costs, regularly rebalanced portfolios. This was in fact one of the major themes of our 2012 book. There are frequently times when diversified portfolios are real bummers. The chart below shows the relative performance of the S&P 500 ($SPY), MSCI EAFE ($EFA) and MSCI Emerging Markets ($EEM) portfolios since the beginning of 2010.

Source: StockCharts

In short, diversifying your equity exposure overseas, especially into the emerging markets has been a big performance drag. That is not however the reasoning behind global diversification. In short, there will always be some asset outperforming, and vice versa. Two prominent bloggers recently touched on this very idea.

Ben Carlson at A Wealth of Common Sense highlighted three reasons to broadly diversify including this:

- No one really knows how the future is going to turn out. The U.S. has been the clear winner over the last century or so in terms of becoming an economic and stock market powerhouse. It’s hard to see that changing anytime soon but who knows how these things will play out in the future from a relative perspective. Diversification is an admission of a lack of foresight about an uncertain future.

Cullen Roche at Pragmatic Capitalism turned things around a little bit and took the perspective of a Japanese-based investor. He shows how home country bias would have badly hurt a Japanese investor’s performance over the past couple of decades. Roche writes:

Having a home bias can expose you to a lack of diversification in your portfolio as it exposes you to too much domestic economic risk. We diversify into foreign markets because we expect the global economy to perform in an uncorrelated fashion over time (as it is now). And this means there will be times when pieces of that portfolio look very bad. But over the course of long periods of time these pieces will tend to have a long-term positive correlation even if the pieces move in an uncorrelated manner in the short-term. The total result is better performance through better diversification.

One of the reasons why advisors recommend not only having a diversified portfolio but rebalancing it on a periodic basis is that it forces investors to buy assets that declined on a relative basis and sell those that gone up in value. As Josh Brown at The Reformed Broker writes:

A diversified strategic portfolio is at all times selling hubris and buying humiliation. It’s not fun while you’re doing it, but it looks great at cycle’s end, when everyone else seems to have been doing the opposite.

For investors who have a crystal ball, portfolio diversification is unnecessary. For the rest of us a globally diversified portfolio tended to on a regular basis provides an opportunity to better handle the vagaries of volatile markets…like those we are experiencing today.