Tuesdays are all about academic (and practitioner) literature at Abnormal Returns. You can check out last week’s links including a look at the state of indexing today.

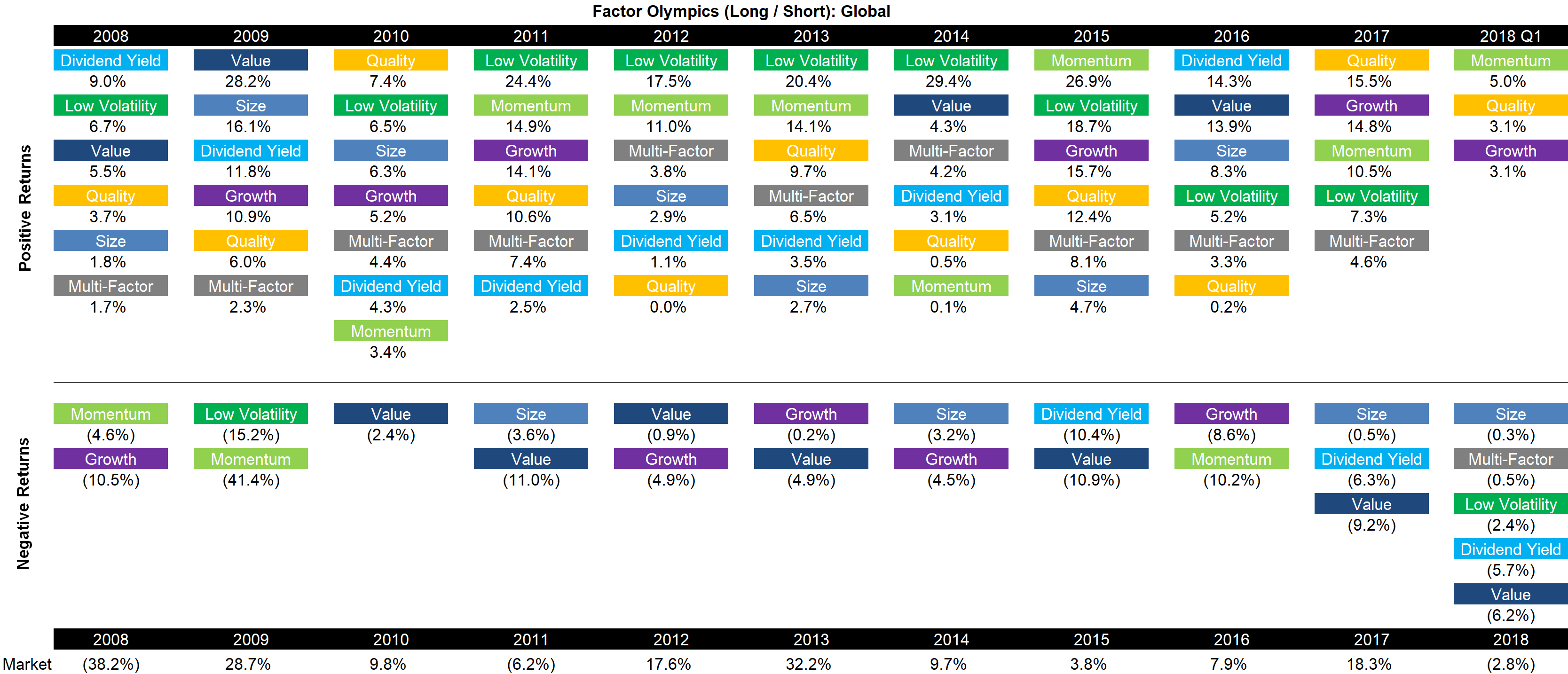

Momentum

- Some common misconceptions about momentum strategies. (dualmomentum.net)

- Momentum profits may be a return to exposure to systemic crash risk. (alphaarchitect.com)

Country selection

- Country valuation metrics haven't worked in awhile now. (alphaarchitect.com)

- A measure of news/sentiment can be used to forecast stock markets around the world. (papers.ssrn.com)

Risk premia

- Does the liquidity premium still exist in listed stocks? (allaboutalpha.com)

- The equity risk premium shows up on days of big macroeconomic announcements. (papers.ssrn.com)

Hedge funds

- Only a small percentage of hedge funds earn alpha after fees. (etf.com)

- The number of successful activist campaigns is pretty steady over time. (institutionalinvestor.com)

Backtests

- Why technical analysis is uniquely prone to overfitting bias. (mathinvestor.org)

- What non-quants need to understand to tell a good backtest from a bad backtest. (marketfox.org)

- 15 common data fallacies. (visualcapitalist.com)

Roundups

- A round-up of recent research articles on portfolio management. (capitalspectator.com)

- Top 20 whitepapers for March 2018. (linkedin.com)

Research

- How much risk do the big Ivy League endowment funds really take? (markovprocesses.com)

- Does tone matter on earnings calls? (blogs.cfainstitute.org)

- On the dangers of DIY TAA. (allocatesmartly.com)

- On the challenges of implementing a tail-risk hedging strategy. (alphaarchitect.com)

- Superstar engineers that go into finance often become disappointed. (papers.ssrn.com)