Tuesdays are all about academic (and practitioner) literature at Abnormal Returns. You can check out last week’s links including a look at the fading power of analyst earnings expectations.

Quote of the Day

"We now think of PwC as a low-probability risk factor that investors should think about, especially in cases where the accounting smells creative."

(Don Bilson, an analyst at investment research firm Gordon Haskett Research Advisors)

Alternatives

- Hedge funds downshifted their risk taking post-GFC. (papers.ssrn.com)

- Three trends that held back hedge fund performance over the past decade. (papers.ssrn.com)

- Why the expected return for private equity investments is falling. (papers.ssrn.com)

- Why is the performance of non-core private real estate strategies so poor? (blogs.cfainstitute.org)

Trend/momentum

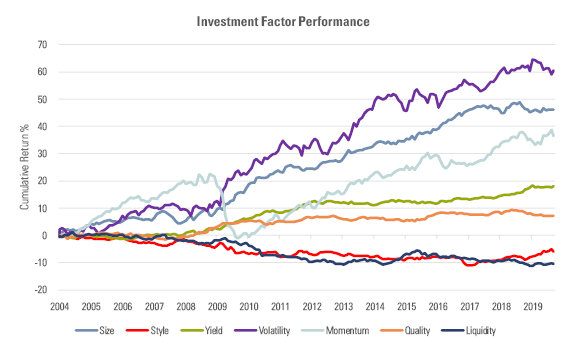

- A look at the history of the momentum factor and its basis going forward. (osam.com)

- Is it possible to improve on simple trend following strategies? (alphaarchitect.com)

- Michael Batnick talks with Corey Hoffstein of Newfound Research about the ins and outs of building trend equity strategies. (theirrelevantinvestor.com)

Research

- There is modest evidence of alpha persistence in active fixed income mutual funds. (morningstar.com)

- Outlining some techniques to improve upon simple deep value screens. (alphaarchitect.com)

- There are significant data issues when it comes to studying ESG performance. (quantpedia.com)

- Savvy Investor Awards 2019: The Best White Papers (savvyinvestor.net)