Tuesdays are all about academic (and practitioner) literature at Abnormal Returns. You can check out last week’s links including a look at whether secrecy helps hedge fund returns.

Quote of the Day

"As with many things in performance accounting and fund marketing, data can be accurate and misleading at the same time."

(Craig Lazzara)

ESG

- Is ESG a standalone return factor? (researchaffiliates.com)

- What happens when you combine ESG and momentum in a portfolio? (quantpedia.com)

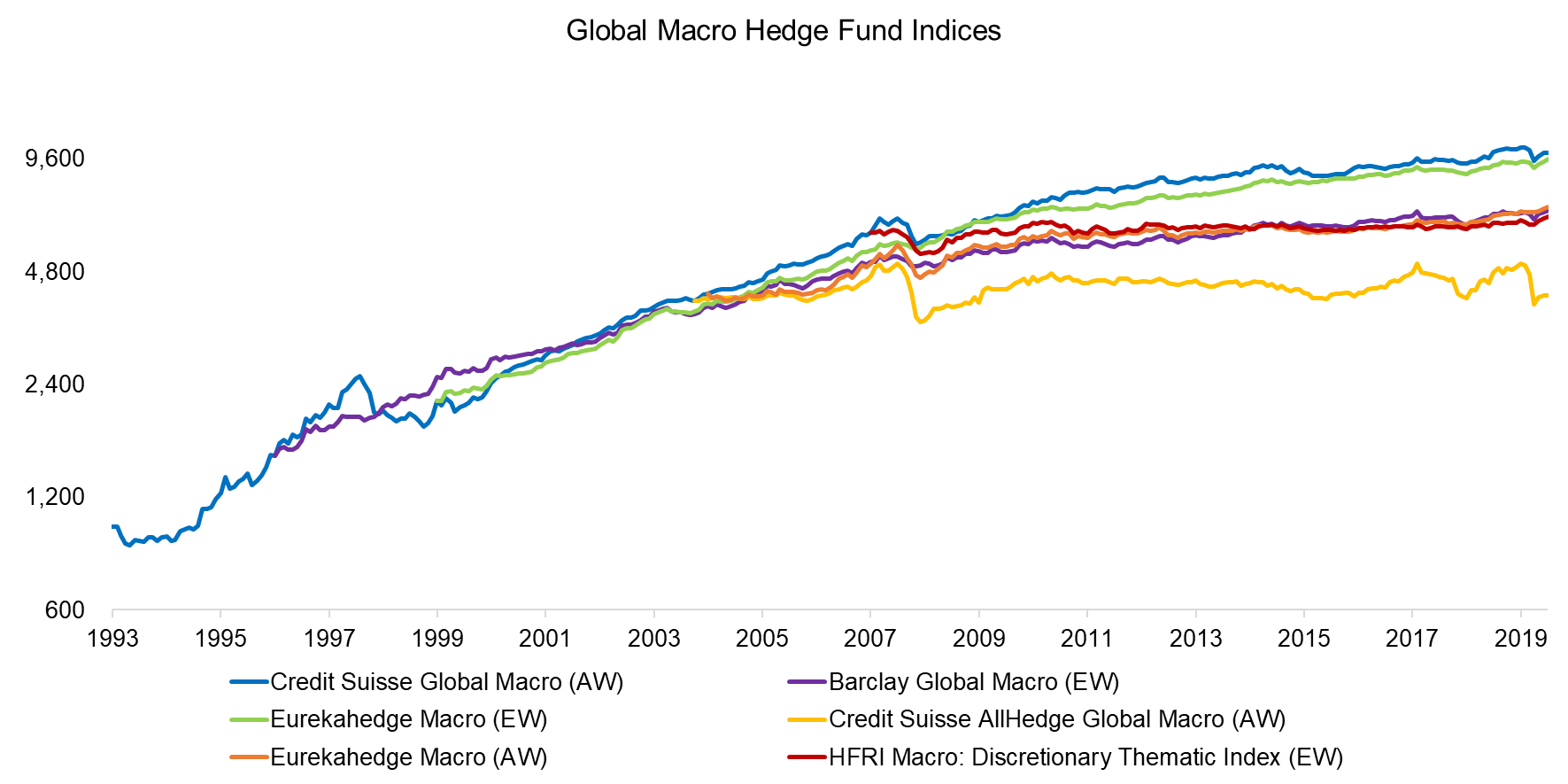

Hedge funds

- Do successful hedge funds possess similar characteristics? (mrzepczynski.blogspot.com)

- Activist hedge funds are good at picking stocks, but not turning around companies. (institutionalinvestor.com)

- The hedge fund industry's standard incentive contract is seriously flawed. (evidenceinvestor.com)

New looks at old data

- Should we give the CAPE ratio another look? (morningstar.com)

- Rotate in May, don't sell: a new look at the seasonality factor. (dualmomentum.net)

- Whatever past return predictability there was with mutual funds is now long gone. (insights.som.yale.edu)

Research

- The past ten year spread between small, cheap stocks and big, expensive stocks is large but not historically unusual. (mailchi.mp)

- Same and different: comparing emerging market equity and emerging bond returns. (factorresearch.com)

- If private equity IRR calculations reflected reality we would all be rich. (ft.com)

- Investors love to login to their brokerage accounts when they have a winner. (klementoninvesting.substack.com)