Tuesdays are all about academic (and practitioner) literature at Abnormal Returns. You can check out last week’s links including a look at the case for Bitcoin in a diversified portfolio.

Quote of the Day

"The current world of low bid-ask spreads and no commissions opens up an array of strategies aimed at capturing the rebalancing premium. The fees and costs no longer overwhelm the premium. Shannon’s Demon is implementable now."

(BTM)

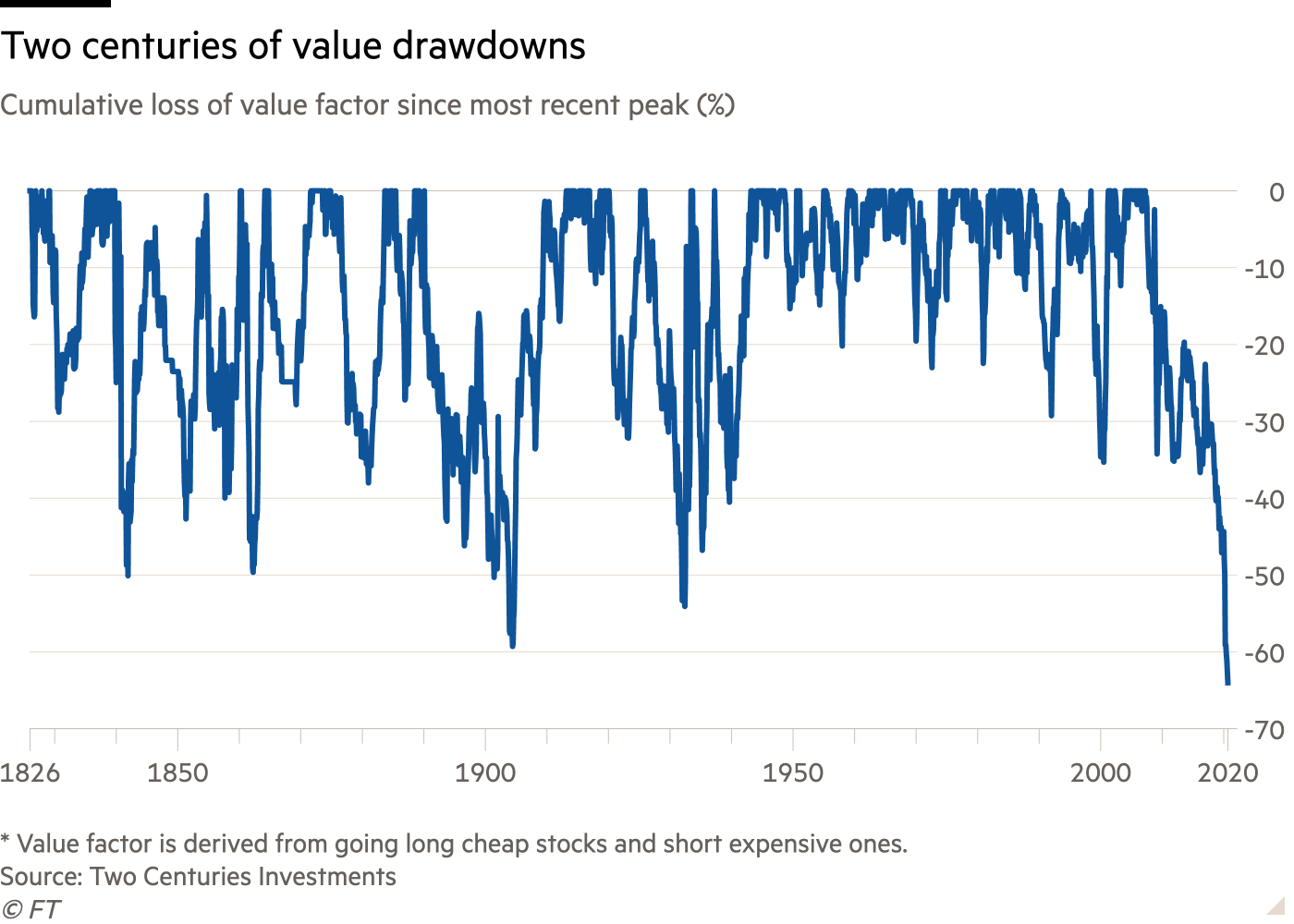

Factors

- The case against the momentum factor. (papers.ssrn.com)

- How free float should affect how we think about what is a small cap stock. (covestreetcapital.com)

- How to fix value investing. (aswathdamodaran.blogspot.com)

Research

- Research shows institutional portfolios are taking all sorts of unintended and uncompensated risks. (institutionalinvestor.com)

- The 2020 Invesco Global Factor Investing Study including a look at ESG adoption. (invesco.com)

- IRR is an imperfect measure of returns and that's okay. (institutionalinvestor.com)