Tuesdays are all about academic (and practitioner) literature at Abnormal Returns. You can check out last week’s links including a look at more evidence showing that day traders, on average, lose money.

Quote of the Day

"Quantitative models have an edge because they will not suffer from the risky shift effect."

(Mark Rzepczynski)

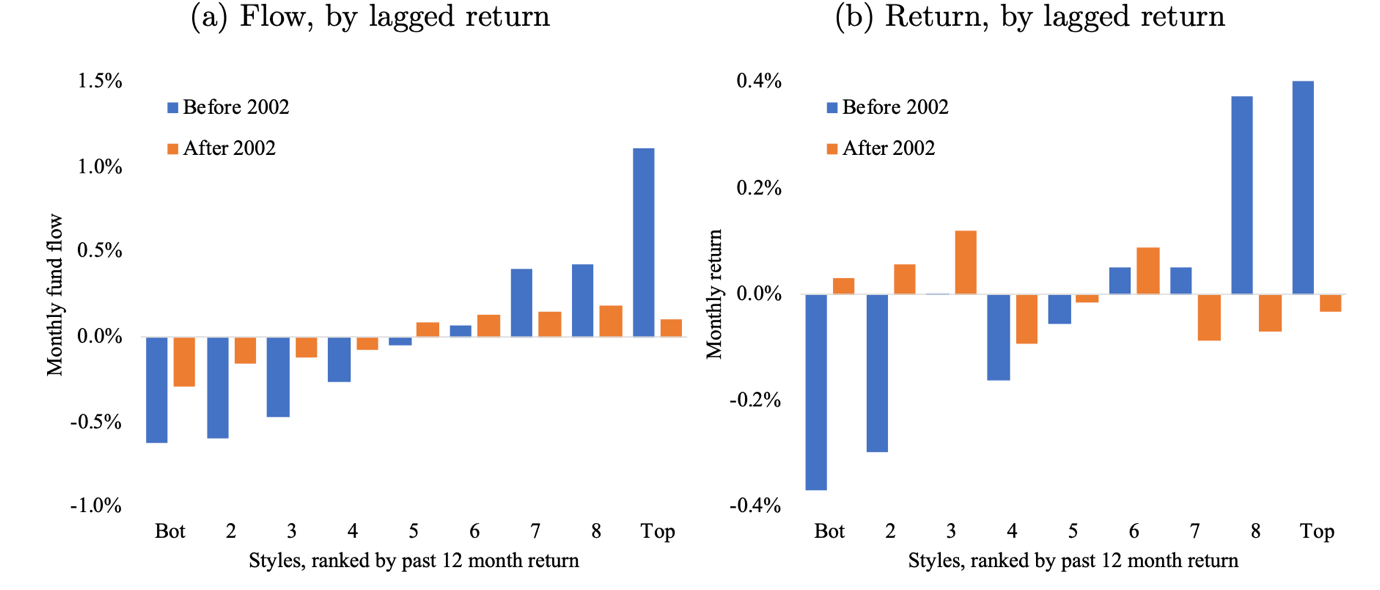

Chart of the Day

How the introduction of Morningstar’s ($MORN) style boxes changed fund flows.

Quotes

- Meb Faber, "Most of the excess returns from the best performing stock periods have come from valuations going from really low back to average or above. (and vice versa)." (mebfaber.com)

- Larry Swedroe, "The conventional wisdom that past performance is a strong predictor of future performance is so strongly ingrained in our culture that it seems almost no one stops to ask if the conventional wisdom is correct, even in the face of persistent failure." (evidenceinvestor.com)

- Johann Colloredo-Mansfeld, "Historically, markets demonstrate a cyclical fallibility. Investors tend to over-extend when heading into bad times and exhibit excessive caution when heading into good times." (mailchi.mp)

Paper

- "Cryptoassets: The Guide to Bitcoin, Blockchain, and Cryptocurrency for Investment Professionals" by Matt Hougan and David Lawant. (cfainstitute.org)

- "Why is Intermediating Houses so Difficult? Evidence from Ibuyers" by Buchak, et al. (privpapers.ssrn.com)

- "A Sober Look at SPACS" by Michael Klausner, Michael Ohlrogge, and Emily Ruan. (corpgov.law.harvard.edu)

Behavior

- Households treat capital gains and dividends differently when it comes to consumption. (alphaarchitect.com)

- Insider trading isn't just for deals any more, now it includes cyberhacks as well. (institutionalinvestor.com)

Research

- Does the small-cap effect show up within the S&P 500? (wsj.com)

- There seems to be momentum in anomaly returns. (alphaarchitect.com)

- Factor analysis is not a one-size fits all situation. (factorresearch.com)

- 12 lessons from a career in quant investing including 'If you have a risk in the book you don’t like, don’t hedge it, sell it.' (man.com)