Tuesdays are all about academic (and practitioner) literature at Abnormal Returns. You can check out last week’s links including a look at how fund companies switch benchmarks to make performance look better.

Quote of the Day

"For investors with long investment horizons and a willingness to tolerate uncomfortable portfolio rebalancing trades, smart beta strategies can help achieve investment objectives. Sadly, mislabelled fund names and the lack of an aligned definition around these strategies mislead and obscure."

(Rob Arnott)

ESG

- On the relationship between ESG ratings and company risk. (evidenceinvestor.com)

- ESG has changed the nature of IPO disclosures. (advisorperspectives.com)

Insights

- Brand is an asset, but the influencer age is changing how brands are made. (sparklinecapital.com)

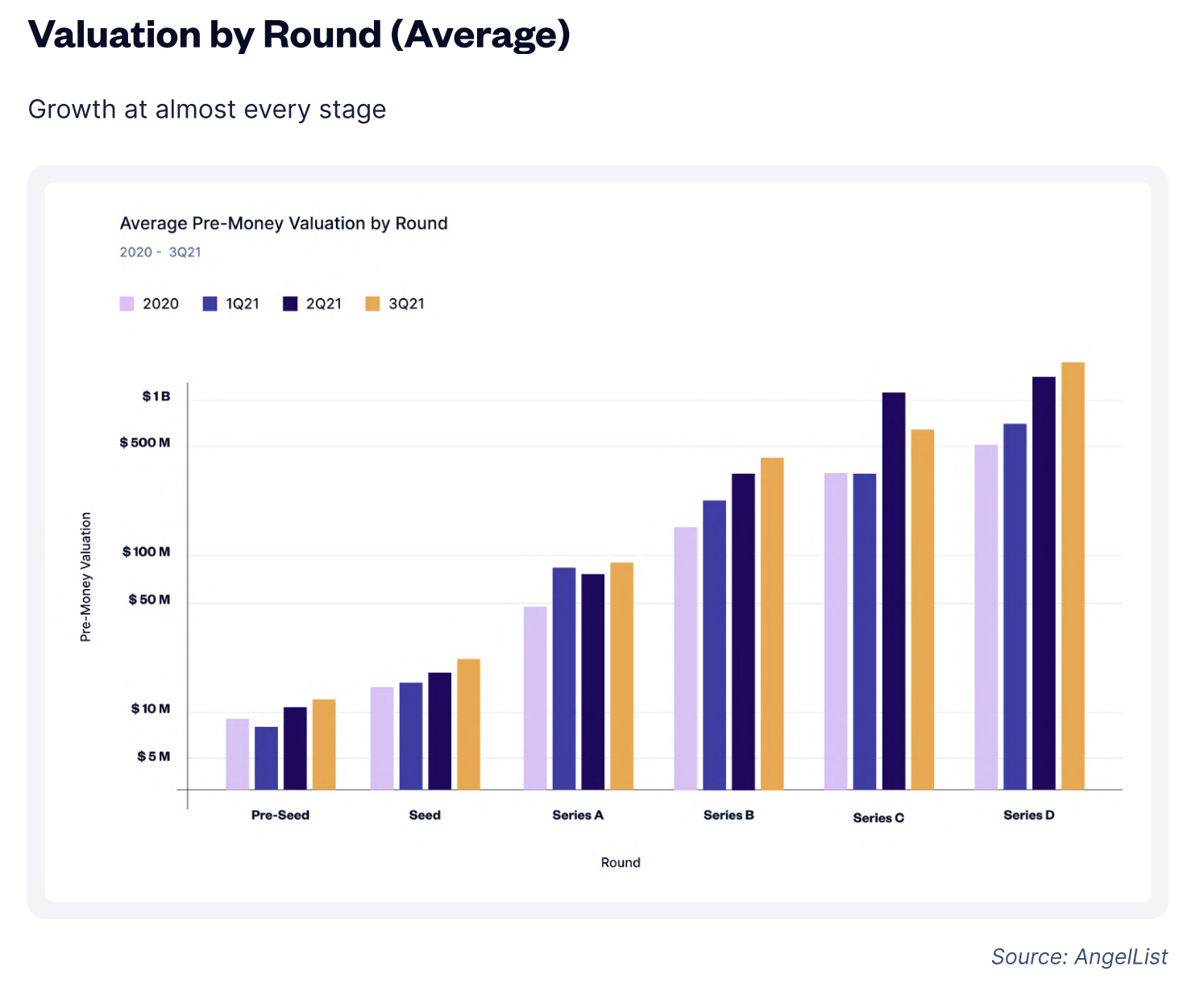

- The State of U.S. Early-Stage Venture and Startups: 3Q21 from AngelList and Silicon Valley Bank ($SIVB). (angellist.com)

Factors

- Comparing the use of asset classes vs. factors in asset allocation. (alphaarchitect.com)

- What factors perform well during high inflation regimes. (canvas.osam.com)

Research

- Why stock market snapbacks during a recession can be so violent. (klementoninvesting.substack.com)

- The case for small cap value in Europe. (mailchi.mp)

- Retail-dominated markets tend to see momentum, vs. mean-reversion. (insights.factorresearch.com)

- How does enhanced fee disclosure change 401(k) member behavior? (alphaarchitect.com)

- A round-up of the past month's research white papers including 'Fair Weather Trends: Seasonality and Google Mobility Data.' (bpsandpieces.com)