Tuesdays are all about academic (and practitioner) literature at Abnormal Returns. You can check out last week’s links including a look at who thematic investors are trading against in reality.

Quote of the Day

"Markets, in their infinite madness, can produce all sorts of delightfully weird anomalies caused by under-appreciated, often boring technical factors, most of which are in practice impossible to exploit but can lead to all sorts of fantastical theories."

(Robin Wigglesworth)

Quant stuff

- On the differences between machine learning and deep learning. (mrzepczynski.blogspot.com)

- A round-up of January's research papers including 'What is the "right" timeframe, if any, to determine a trend?' (bpsandpieces.com)

- The basics of factor models. (sr-sv.com)

Volatility

- On the value of the VIX futures premium as an indicator. (alphaarchitect.com)

- Can the VIX add value to the term spread in forecasting the economy? (quantpedia.com)

Behavior

- Underreaction helps explain the momentum effect. (papers.ssrn.com)

- Poor financial literacy is associated with inertia. (papers.ssrn.com)

- Acquisitions are stressful for employees. (papers.ssrn.com)

Research

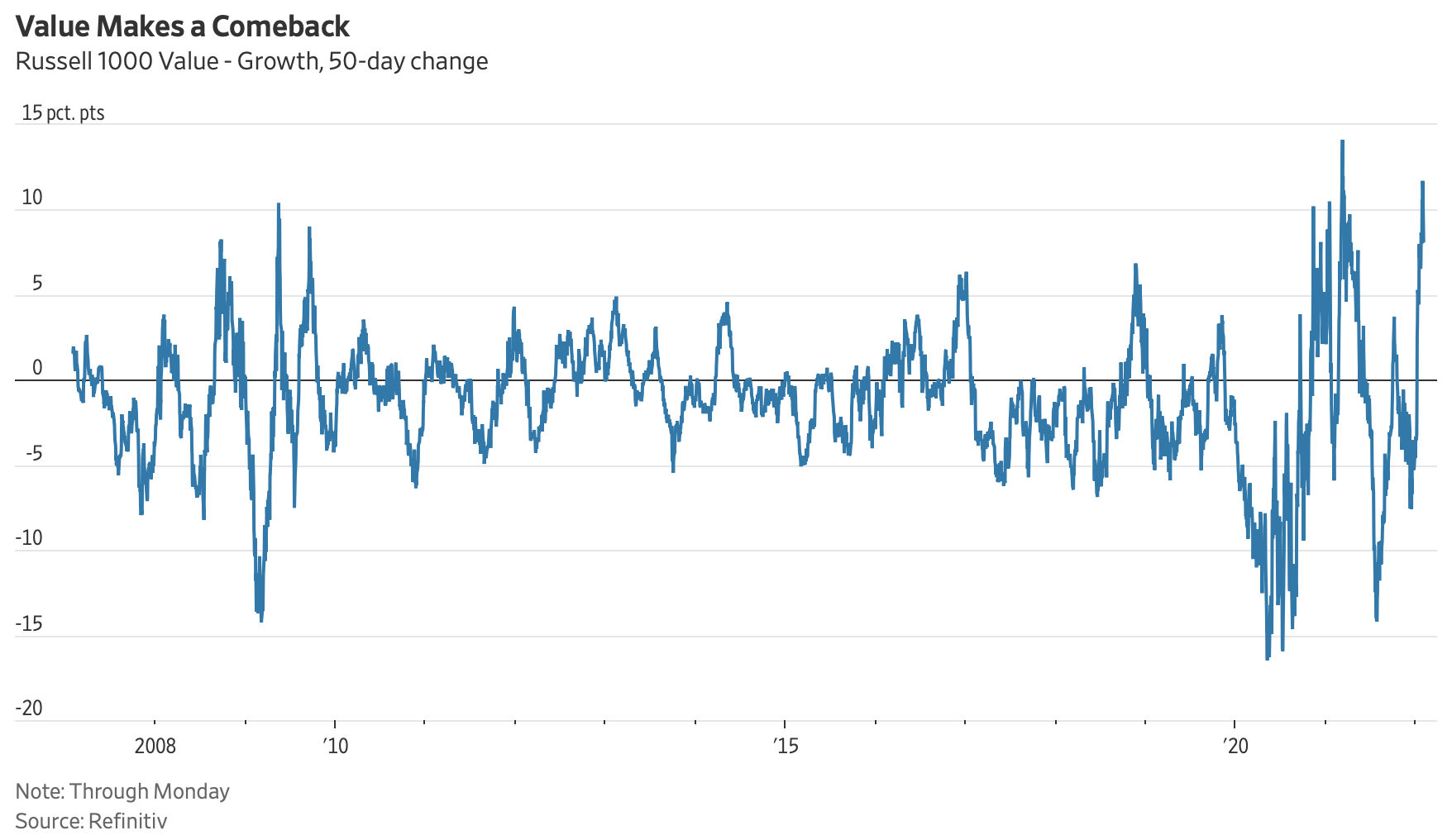

- Why the fall in growth stocks has a ways to go. (mailchi.mp)

- How TAA strategies performed during the worst pullbacks. (allocatesmartly.com)

- Crypto hedge funds have benefited from the surge in cryptocurrencies. (insights.factorresearch.com)

- Does private real estate have a return advantage over public REITs? (evidenceinvestor.com)

- How short-seller attacks with price targets play out. (klementoninvesting.substack.com)