Tuesdays are all about academic (and practitioner) literature at Abnormal Returns. You can check out last week’s links including a look at the poor forecasting ability of active share.

Quote of the Day

"In sum, PE LPs are paying higher-than-S&P 500 prices for near-distressed credit quality micro-caps with a heavy sector bias toward tech and healthcare."

(Dan Rasmussen)

Diversity

- Some evidence that gender diversity helps fund performance. (papers.ssrn.com)

- What role does race play in manager selection? (alphaarchitect.com)

Indexing

- What happens when stocks are added/deleted from the S&P 500? (papers.ssrn.com)

- Managing a passive fund is not a push button exercise. (nber.org)

Market timing

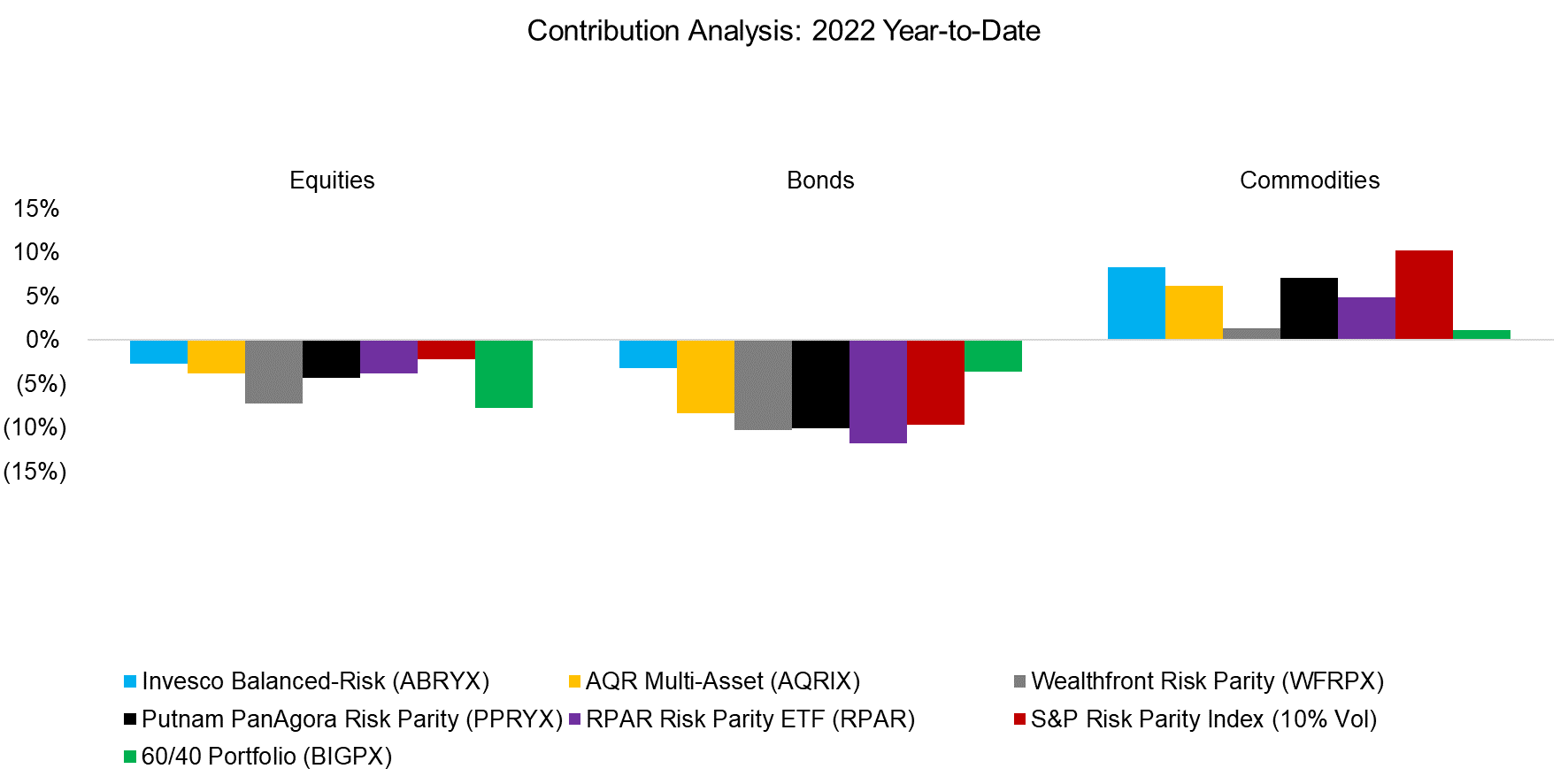

- Why 2022 has been unusual for anyone doing tactical asset allocation. (allocatesmartly.com)

- More evidence that trying to forecast the market is futile. (klementoninvesting.substack.com)

Research

- Time series momentum works but can go through long periods of underpeformance. (alphaarchitect.com)

- Low-risk stocks earn their outperformance during bear markets. (robeco.com)

- Why value investors would do well to look overseas. (alphaarchitect.com)

- How companies with intangible assets react to higher interest rates. (klementoninvesting.substack.com)

- Flows matter over the short run. (blog.validea.com)

- How factors are defined matter. (quantdare.com)