Tuesdays are all about academic (and practitioner) literature at Abnormal Returns. You can check out last week’s edition including a look at the crash risks of crowded trades.

Quote of the Day

"Factors aren’t laws of physics, but they are a handy framework for understanding markets."

(Robin Wigglesworth)

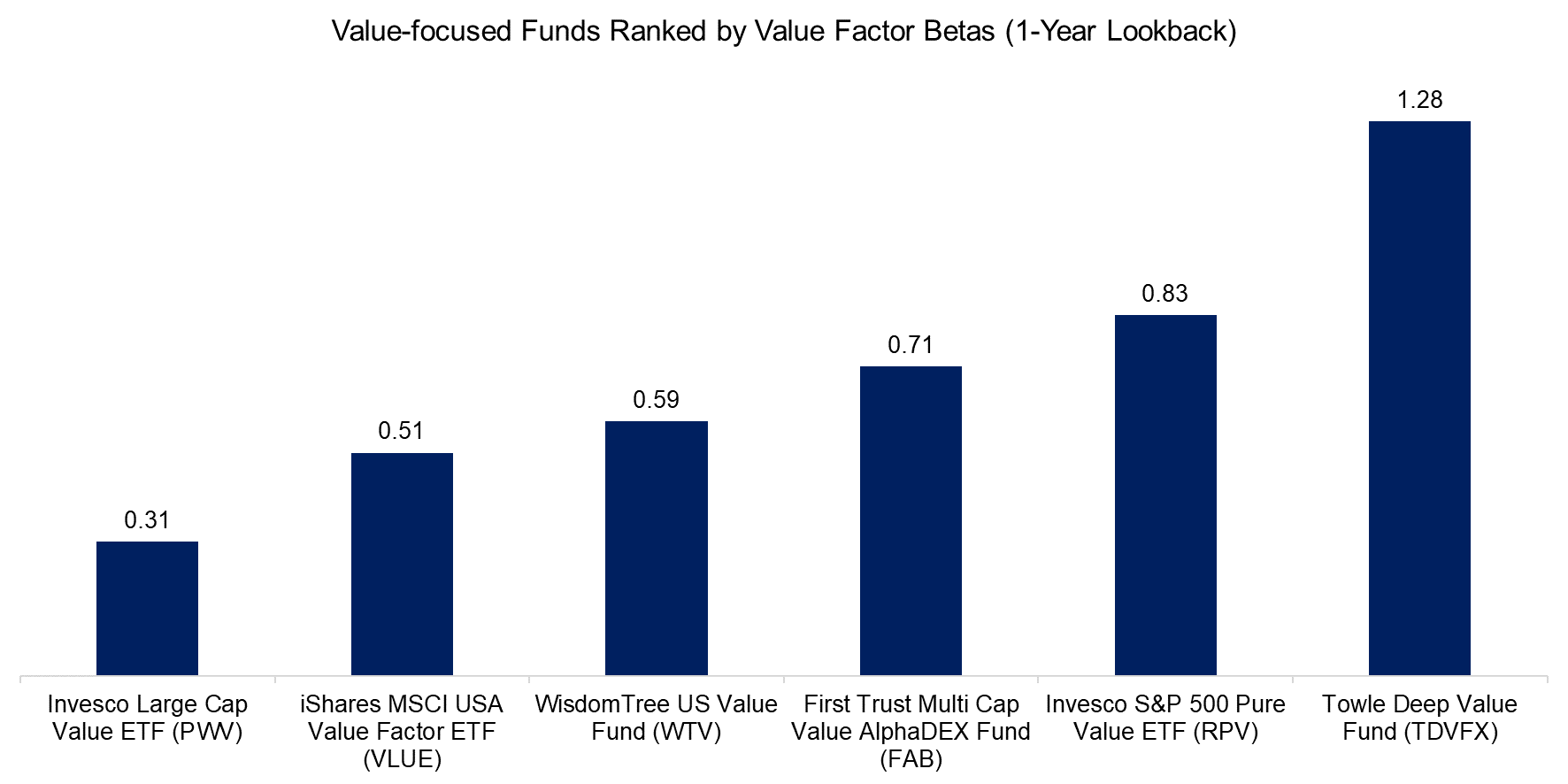

Chart of the Day

Value factor exposure varies widely among value (and non-value) funds.

Asset management

- Big asset managers get paid on AUM, not performance. (papers.ssrn.com)

- A primer on private credit. (sapientcapital.com)

- How the ETF came to be. (institutionalinvestor.com)

Macro

- There seems to be a macroeconomic announcement premium. (papers.ssrn.com)

- What effect do demographics have on real interest rates? (papers.ssrn.com)

- Media (economic) sentiment has gotten increasingly negative over the past 50 years. (papers.ssrn.com)

Households

- How market moves affect household investment behavior. (papers.ssrn.com)

- Do ESG disclosures affect consumer behavior? Only mildly... (papers.ssrn.com)

Research

- Kai Wu, "Trademarks provide a useful tool for finding strong brands." (sparklinecapital.com)

- Just how useful is capital markets data from the 19th century? (morningstar.com)

- Insider buys are more informative than insider sells. (papers.ssrn.com)

- Institutional investors sniff out deals which are accretive to the acquirer. (papers.ssrn.com)

- The case for more 'behind the scenes' small cap activism. (blogs.cfainstitute.org)

- A review of recent research on fail-tailed distributions. (capitalspectator.com)