Tuesdays are all about academic (and practitioner) literature at Abnormal Returns. You can check out last week’s links including a look at whether low vol is just ‘value in disguise.’

Quote of the Day

"No financial researcher agrees on the canonical set of factors or how best to proxy them."

(Eric Falkenstein)

Quant stuff

- The future of finance is data, not models. (mathinvestor.org)

- 16 quants, including Cliff Asness, talk about the future of quantitative investing. (bloomberg.com)

- Moving averages 101. (sentimentrader.com)

Factors

- Why Ken French isn't willing to write-off the value premium yet. (institutionalinvestor.com)

- A look at how investor sentiment affects factor returns. (factorresearch.com)

- Crowding is a real issue with alternative risk premia. (alphaarchitect.com)

Behavior

- Incentives matter when it comes to financial sales. (alphaarchitect.com)

- People like to consume out of capital gains. (papers.ssrn.com)

Research

- Another reason to separate alpha and beta: tax efficiency. (cfainstitute.org)

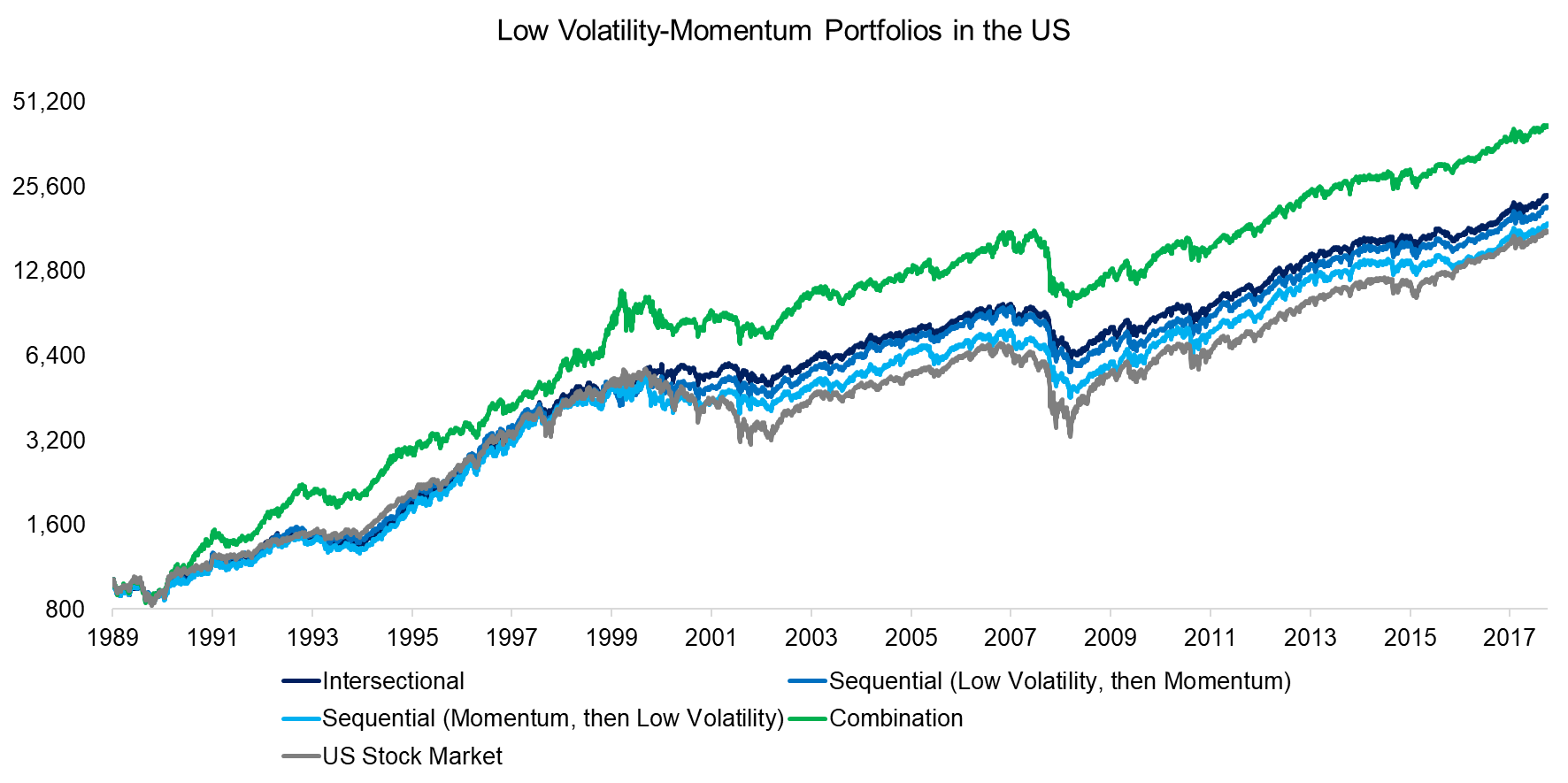

- Darren Horn, "Replacing time-series momentum in individual stocks/futures contracts with cross-sectional momentum plus a time-varying exposure to the market may be easier to conceptualize and simpler to explain to others." (alphaarchitect.com)

- An example of where lower fund fees leader to better performance. (cfainstitute.org)

- Powerful CEOs equal a greater risk of a stock price crash. (sciencedirect.com)

- John Maynard Keynes was a good art collector, to boot. (academic.oup.com)