Drawdowns happen. Sometimes they happen in absolute terms, think the S&P 500 down 50% in 2008-09. Sometimes they happen in relative terms, think value stocks in 1999-2000. Sometimes they happen in time, think managed futures from 2009-2914. In all cases drawdowns, either absolute or relative, represent a psychological challenge for investors.

As I discuss in my book, and in this Q&A with Wes Gray of Alpha Architect, it is difficult to be a value or momentum investor because both styles undergo periods of significant underperformance. The psychological pressure on investors during these periods is significant and can unseat them from their chosen strategy.

After a nearly six year bull market in domestic stocks and a unusually long time since a 10% correction it feels like risk has been banned from the stock market. However investors should take a look at history to remind themselves that drawdowns happen. As Ben Carlson at A Wealth of Common Sense writes:

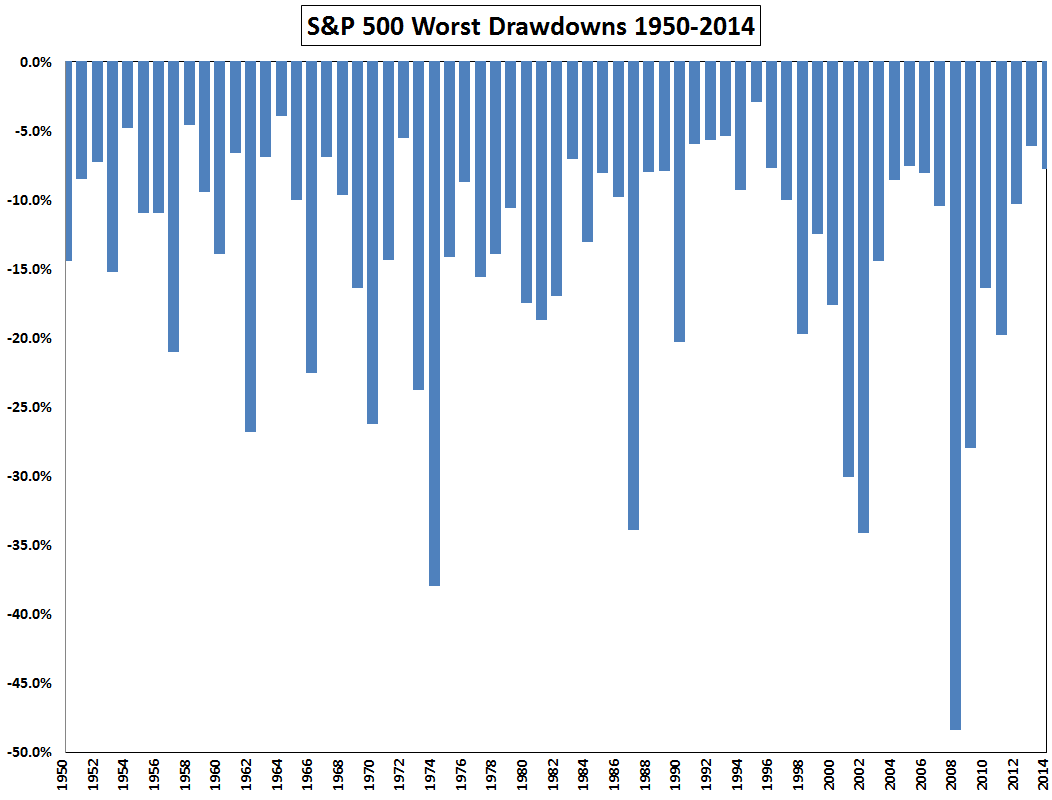

Losses are a normal part of a well-functioning market. Without occasional losses, stocks wouldn’t earn a risk premium over safer asset classes such as bonds and cash. Take a look at this chart I made which details the worst drawdowns* on the S&P 500 every single year since 1950:

You can see that losses are perfectly normal. They happen. Get used to it. There were only four years — 1954, 1958, 1964 and 1995 — where stocks didn’t have a least a 5% correction at some point during the year.

In other words, risk premiums exist for a reason. Investors are required to experience risk, i.e. drawdowns, from time to time. Each cycle is different but they all at some point punish investors. As David Merkel at the Aleph Blog writes:

Risk premiums aren’t free money — eggs from a chicken, a cow to be milked, etc. (Even those are not truly free; animals have to be fed and cared for.) They exist because there comes a point in each risk cycle when bad investments are revealed to not be “money good,” and even good investments are revealed to be overpriced.

Risk premiums exist to compensate good investors for bearing risk on “money good” investments through the risk cycle, and occasionally taking a loss on an investment that proves to not be “money good.”

Who knows when the next 10% correction, or 20% bear market will occur. I am sure Jesse Felder would like the prior to happen sooner rather than later. In any event it is good to remind ourselves of these facts before they occur rather than during the drawdown. Because when the actual drawdown happens you will have other things on your mind.