A couple weeks ago Jason Zweig at WSJ wrote a personal and moving piece on selling the home where he was raised and where his mother had lived until recently. His experience is at-odds with the thinking of many Millennials who do not want to be weighed down by the cost and responsibility of owning a home. Zweig concludes his piece:

A home is more than an investment. It is the place that helps shape who we are. Your generation may well be thankful that you don’t have to bear the burdens of owning one — the mortgage, the maintenance, the pain of pulling up roots that run decades deep. My generation, and my mother’s, are thankful we had the blessings.

A home is often a blessing but it is not an investment. In a follow-up piece Zweig attempts to calculate the return on the aforementioned house and comes up with a disappointing number. He writes in a piece at MoneyBeat:

..I can make only a guess at their rate of return between 1961, when they bought, and this past week, when my mom sold. My very rough estimate is that it amounts to a rate of return of about 4% annually, roughly equivalent to the rate of inflation over the same period — in other words, a real return fractionally better than zero. Account for the money they might otherwise have incurred in rent, and the return would be slightly higher.

On the other hand, once you factor in repairs, routine maintenance and annual property taxes along the way, plus commissions and other costs on the final sale, the return after inflation would be negligible or even negative.

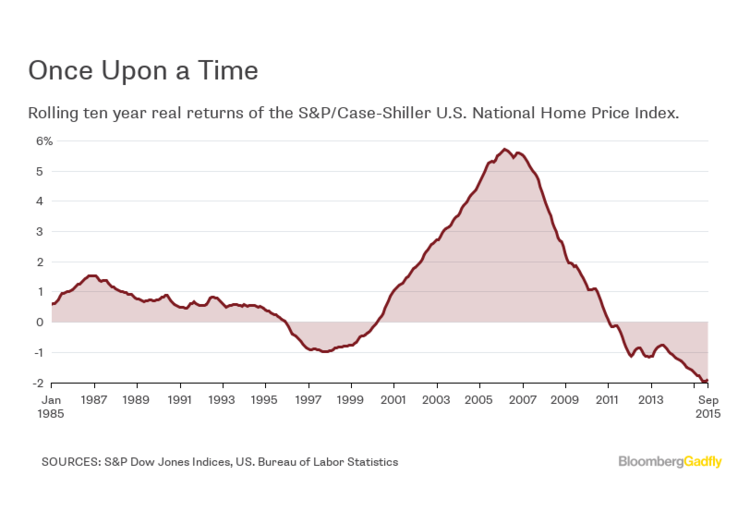

This result of moderate to negative real returns is in line with the Case-Shiller numbers on home price returns. Nir Kaissar at Bloomberg included the graph below to demonstrate that over time, except for a brief period during the housing bubble of the early 2000s, houses on a national basis have generated low positive real returns.

Source: Bloomberg

Despite the relatively poor performance of homes, Kaissar notes there is a persistent myth that homes are solid investments. For example the Case-Shiller indices don’t take into account the many other costs involved in home ownershiop. He like Zweig recognize there are non-financial reasons to own a home but there are much better ways to invest in real estate. Kaissair concludes:

There are numerous non-financial benefits, and some personal financial benefits (the mortgage interest deduction, for example) to buying a home. But if you want diversification, and if you want meaningful expected price appreciation from real estate, buy a REIT and rent your home. Homes are wonderful places to raise a family. They aren’t great investments.

One of the reasons why homes may be such a hot investment is that Americans continue to demand ever larger houses, and for now, home builders are willing to accommodate that demand. Rani Molla also at Bloomberg notes why builders are chasing the McMansion crowd but notes the eventual downside of focusing on an increasingly small demographic niche.

As noted above there are a number of reasons to own a home that have nothing to do with the dollars and cents of it all. It probably makes more sense to think about homes as assets and not investments. For instance, today it is easier than ever for those in retirement to get a reverse mortgage on their home to fund their ongoing needs for income. Scott Burns at AssetBuilder notes now the thinking has changed on reverse mortgages.

In my book I make this same distinction between asset and investment in regards to cash or more accurately cash equivalents like money market funds. I wrote:

Cash is an asset, but not an investment. On the face of it, this seems like a false distinction. In this formulation, an asset is anything of value. An investment, on the other hand, is something that is expected to produce real, after-tax returns over time. In this light, cash is something we should value, but we should not expect it to provide us with real returns over time, as should equities or bonds.

It is ironic that two assets that are so different like cash equivalents and a home would generate negative, real returns over time. But if you think a little bit more about it you can see these are two assets that have demands that have nothing to do with their prospective returns. Cash is held by highly risk-averse investors who are, by and large, price-insensitive. Since the outset of the financial crisis cash equivalents have had highly negative real returns but investors continue to hold significant balances.

The demand for homes is driven a whole host of factors that have nothing to do with prospective returns. There is nothing like a birth (or two) to prompt a couple to look for a larger home. Homes have in econspeak non-pecuniary benefits, or benefits that can’t be measured by money.

Zweig may very well be right that the latest generation will miss out on these benefits if they eschew home ownership. A better bet is that they come around to home ownership as they make a demographic transition. However they would be wise to think about their home as an asset and not an investment. Otherwise every call to the plumber or HVAC technician will feel like a loss and not a chance to keep your family warm and dry.