Tuesdays are all about academic (and practitioner) literature at Abnormal Returns. You can check out last week’s links including a look at the dangers of using historical returns data in asset allocation.

Quote of the Day

"The problem with historic fund performance is that it is devoid of context and impacted by a blizzard of variables over which the manager has no control."

(Joe Wiggins)

Asset allocation

- Tactical strategies aren't for everybody, but who are they for? (blog.thinknewfound.com)

- How adding a managed futures sleeve can increase safe withdrawal rates. (papers.ssrn.com)

Alpha

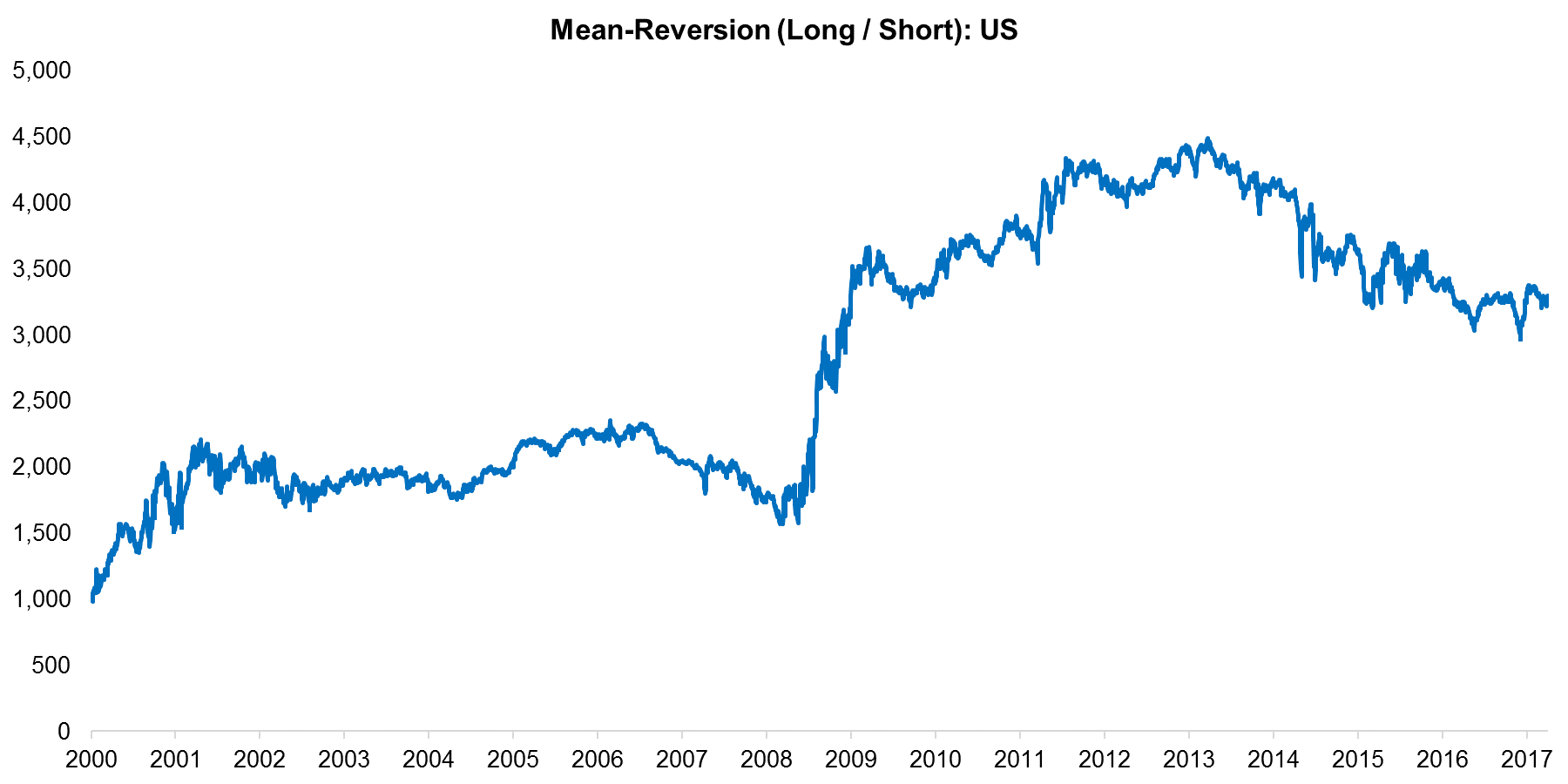

- The "Frustrating Law of Active Management" states: For any disciplined investment approach to outperform over the long run, it must experience periods of underperformance in the short run. (blog.thinknewfound.com)

- "Do index buyers make overvalued stocks more overvalued?" (iijournals.com)

- More evidence that available alpha is shrinking. (etf.com)

Membership

Research links

- If individual stock returns skew negative what is an investor to do? (alphaarchitect.com)

- On the case for tail-risk insurance in a late-bull market. (cambriainvestments.com)

- It's hard to find a consistent relationship between the US dollar and stocks. (fortunefinancialadvisors.com)

- How to sell a business tax efficiently via structured installment sales. (alphaarchitect.com)

- Having social capital pays off for companies during times of crisis. (alphaarchitect.com)