Tuesdays are all about academic (and practitioner) literature at Abnormal Returns. You can check out last week’s links including a look at whether low vol strategies can be improved upon.

Quote of the Day

"Thus, low-beta/low-volatility investing, in and of itself, is not a bad idea. However, if one already has an allocation towards the investment and profitability factors, a low-beta portfolio probably adds little to the portfolio."

(Jack Vogel)

Research

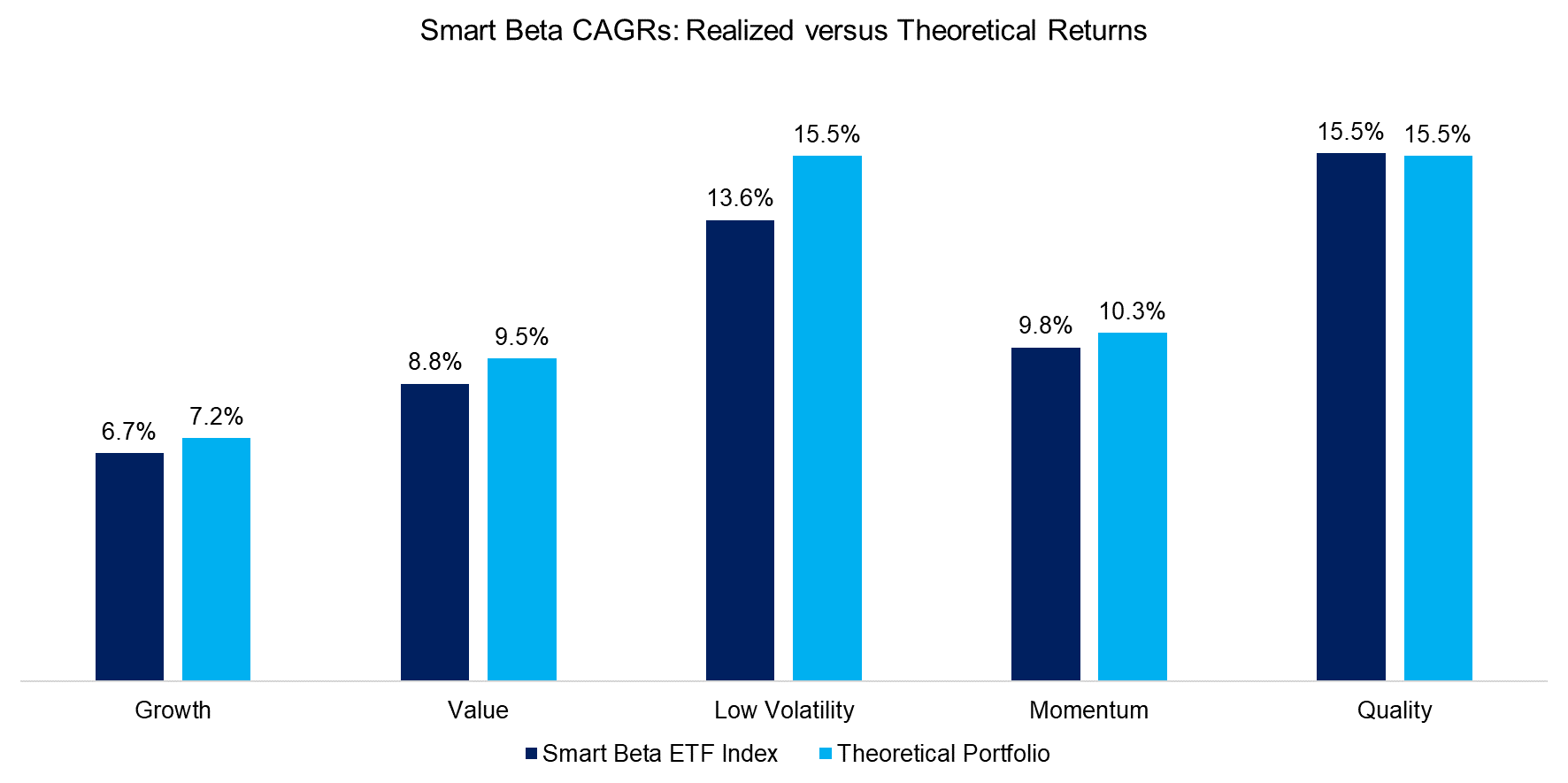

- Six common misconceptions about factor-based strategies. (blog.validea.com)

- How to construct a long-only bond risk premium factor. (blog.thinknewfound.com)

- Some support for the idea of putting more into equities with a long time horizon. (alphaarchitect.com)

- Why low rates (and returns) may be here to stay. (awealthofcommonsense.com)

- High active share is irrelevant if you don't have any actual skill. (alphaarchitect.com)

- Hedge fund managers with a lot of 'skin in the game' tend to keep their funds smaller. (institutionalinvestor.com)

- Companies with an extroverted CEO have a higher cost of equity capital. (wsj.com)