Tuesdays are all about academic (and practitioner) literature at Abnormal Returns. You can check out last week’s links including a look at the difference between machine learning and deep learning.

Quote of the Day

"You and I buy stocks during the day because a) that is when markets are open, and 2) we expect prices to rise over years and decades; we don’t buy because we expect a higher print by 4 pm."

(Barry Ritholtz)

Books

- Ten good books about statistics including "The Art of Statistics" by David Spiegelhalter. (timharford.com)

- An excerpt from Christopher Schellling's book "Better than Alpha: Three Steps to Capturing Excess Returns in a Changing World." (institutionalinvestor.com)

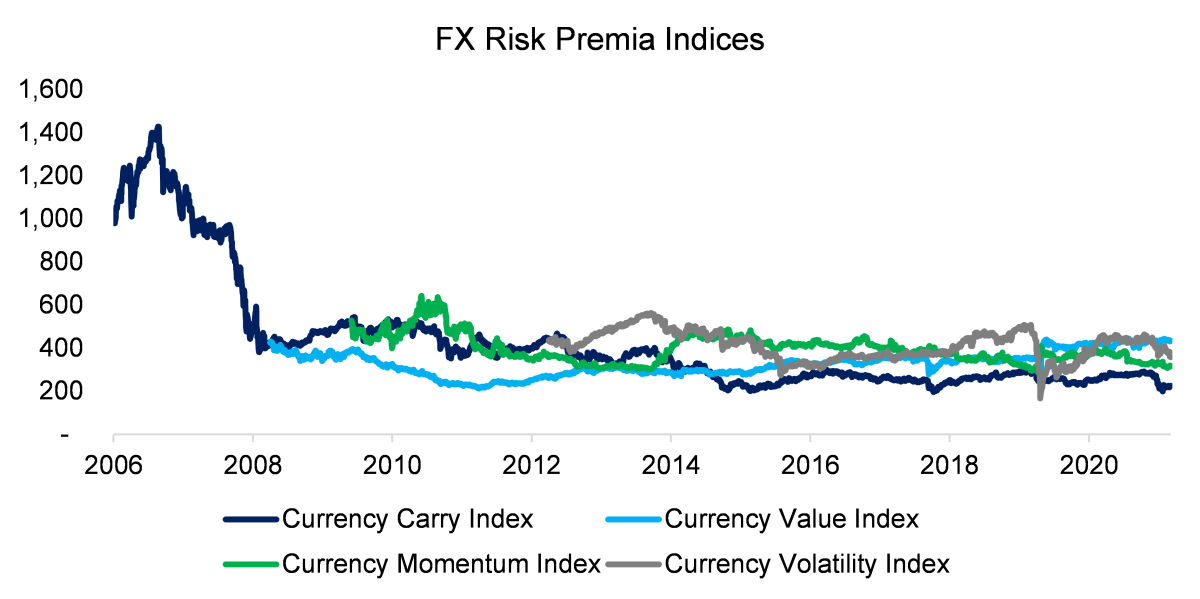

Quant stuff

- What constitutes the 'long run' when it comes to financial data? (klementoninvesting.substack.com)

- Overfitting and the post-hoc probability fallacy. (mathinvestor.org)

Diversity

- Companies led by female CEOs are more likely to be targeted by activists. (wsj.com)

- The role race plays in portfolio decision making. (papers.ssrn.com)

- The gender gap in academic finance is still wide. (alphaarchitect.com)

Factors

- Factors can perform differently in bull and bear markets. (quantpedia.com)

- This hypothesis seems to best explain the momentum factor. (alphaarchitect.com)

- Why factor diversification is important in bear markets. (mrzepczynski.blogspot.com)

- Value stocks have a bigger, negative loading on momentum than originally thought. (alphaarchitect.com)

Research

- Stocks favored by retail traders really do have more crash risk. (evidenceinvestor.com)

- You can't talk about tail risk hedges without talking about their costs. (breakingthemarket.com)

- How risk parity strategies generate a rebalancing premium. (investresolve.com)

- An introduction to dollar-cost averaging strategies. (quantpedia.com)

- Beware the hype when it comes to AI-powered ETFs. (insights.factorresearch.com)

- The Fed does pay attention to the stock market. (alphaarchitect.com)